Understanding Cash Flow Statements

Whether you're a seasoned CPA or an aspiring one, it's no secret that cash flow statements can often appear complex and daunting. This article is designed to unravel this intricacy, presenting a more straightforward understanding of the cash flow statement under US GAAP accounting, supplemented with practical examples.

The cash flow statement fundamentally exhibits the inflows and outflows of cash during a particular period - typically a year. Under the accrual method of US GAAP accounting, it's essential to reflect all transactions on a cash basis, providing a more transparent snapshot of the company's financial health. The cash flow statement is traditionally divided into three primary sections: Operating Activities, Investing Activities, and Financing Activities.

To help you with cash flows, at the bottom of this page, I will include a cheat sheet you can use to solve any cash flow question!

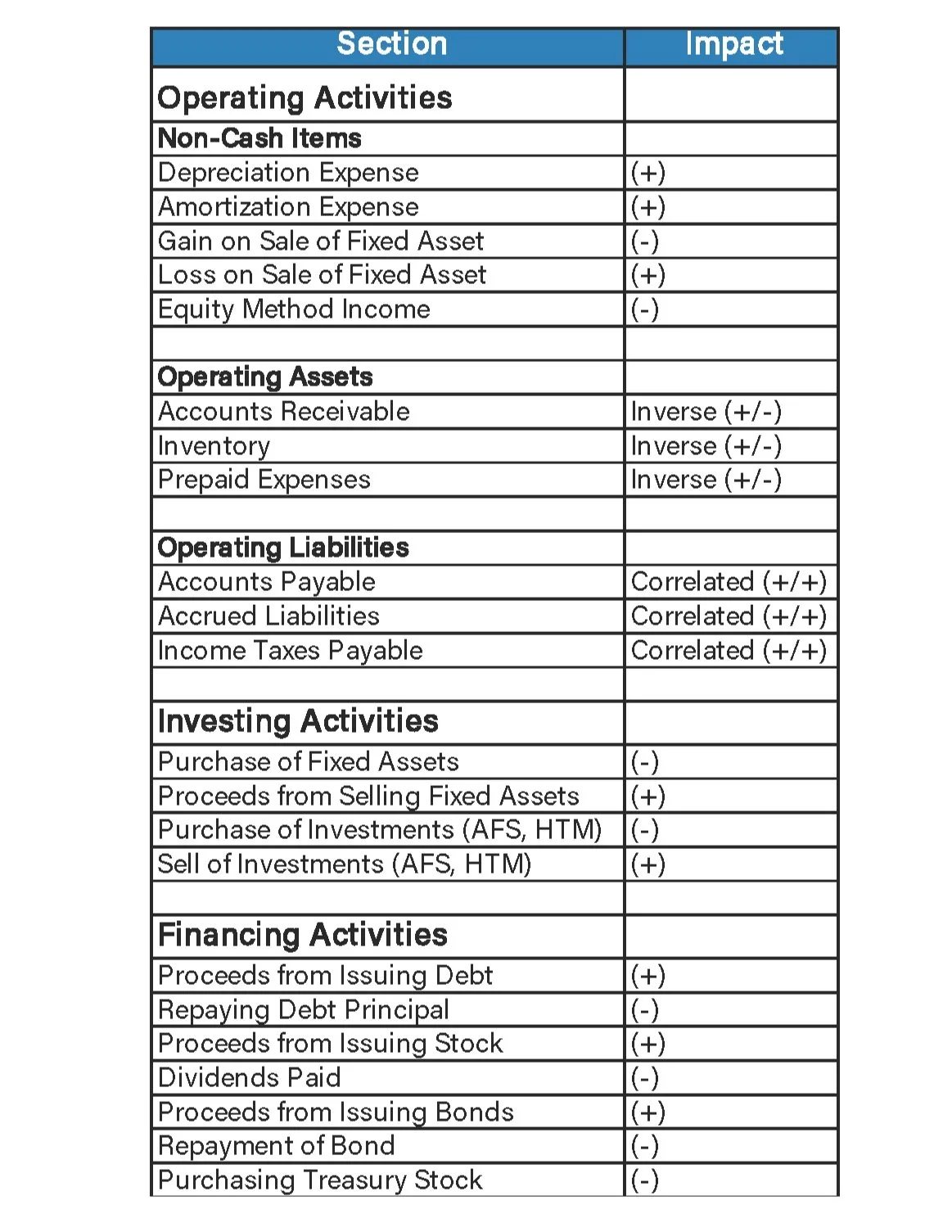

Operating Activities

The Operating Activities section essentially encompasses the company's main operations. The indirect method, predominantly used here, commences with the net income, following which items that are non-cash transactions are reversed. For instance, the depreciation expense, despite reducing net income, doesn't involve an actual cash payout. Therefore, it's added back to the net income.

Investing Activities

Investing Activities involve transactions where cash is spent on investments. This predominantly includes long-term assets, with the most common examples being the purchase and subsequent sale of fixed assets. It's essential to remember that any entries that follow the initial transaction belong to the same section, hence both the purchase and sale of a fixed asset fall under Investing Activities.

Financing Activities

The Financing Activities section encapsulates instances where cash is raised, whether by taking a loan (crediting the loan account) or issuing equity (crediting the equity account). For instance, if equity is issued, the original transaction is logged under Financing Activities. Similarly, when dividends are paid out, they are recorded in the same section, keeping the transactions consistent.

Fixed Asset Impact on Cash Flow Statement

Fixed assets affect the cash flow statement every year. Therefore, it’s important to understand how fixed asset purchases and sales affect the cash flow statement.

Suppose a company sold a piece of machinery for $45,000 cash on September 15th, year three.

The machinery was initially purchased in year one for $60,000 and had accumulated depreciation of $25,000. The net book value of this asset, therefore, was $35,000 ($60,000 - $25,000), resulting in a gain of $10,000 ($45,000 - $35,000).

When the machinery was initially purchased, cash was credited for $60,000, indicating an outflow in Investing Activities. Consequently, when the machinery was sold, the cash inflow was also recorded in the same section. The sale of this machinery involved receiving $45,000 cash, crediting the machinery for its initial value, and debiting the accumulated depreciation, with the gain being the remaining amount.

This gain of $10,000 increases the net income, and the cash proceeds of $45,000 act as an inflow to the Investing Activities section. To prevent double counting, we subtract the gain from the net income under the Operating Activity section, ensuring that the entire amount of proceeds ($45,000) is solely recorded in the Investing Activities section.

Journal Entry for Selling the Fixed Asset

Conclusion

In conclusion, the cash flow statement is a powerful tool for financial analysis and understanding the liquidity position of a business. The key is to accurately categorize and account for all transactions in their respective sections, while simultaneously accounting for non-cash items. A well-drafted cash flow statement, therefore, provides a comprehensive view of a company's financial health, a crucial piece of information for stakeholders, and decision-makers.

Cash Flow Summary Chart